Blue Monday, the day December credit card statements arrive, is coming and that debt won’t pay itself

Article content

Article content

Article content

![]() Blue Monday, the day when Canadians get their December credit card statement, will likely land with a thud on Jan. 20.

Blue Monday, the day when Canadians get their December credit card statement, will likely land with a thud on Jan. 20.

Credit card debt has been growing since interest rates started to climb in 2022, and it rose 9.4 per cent year over year in the third quarter, according to the most recent report from Equifax Inc., due to both population growth and an increase in average balances for people unable to pay in full.

Advertisement 2

Article content

“While recent rate cuts have alleviated some of the strain for some people, the financial pressures on Canadians remain significant,” Rebecca Oakes, vice-president of advanced analytics at Equifax Canada, said in a press release.

But there are ways to cope with the fallout instead of stoking already high levels of financial worry.

One remedy to heal broken finances, say TikTok users, is a no-spend January or year. The social media feed is full of mostly young women taking up the no-spend challenge to try to get a handle on their finances as part of a new year’s resolution or to dig themselves out of overspending during the holidays.

Of course, the no-spend tactic varies by person. Some set a goal of accumulating as many no-spend days — excluding necessities — in a month as possible, similar to going on a diet and keeping within the calorie limit. Others created no-spend lists for January or the rest of the year that run the gamut from cutting out extra toys for their cat and makeup to not going out to clubs or for dinner — taking a scorched earth approach to daily living.

Elevated financial anxiety could explain some of the more extreme approaches to controlling spending.

Posthaste

Article content

Advertisement 3

Article content

Almost 70 per cent of Canadians harbour anxiety when it comes to debt and trying to pay it off, according to a survey by insolvency trustee Harris & Partners Inc.

The survey, which looked at how Canadians are coping with managing their non-mortgage debt, uncovered some “real-life struggles” in dealing with credit card and personal loan debt.

For example, half of the nearly 2,000 people surveyed said they feel stressed managing their debt, while 40 per cent said debt was taking a toll on their family relationships and a bit more than half said they had borrowed money over the past two years to pay for essentials such as food, rent and utilities. Just under a quarter said they did not have $500 on hand to cover an emergency.

“Debt stress is a silent burden carried by millions of Canadians,” Joshua Harris, an insolvency trustee at Harris & Partners, said in the report. “For some, it’s about making ends meet; for others, it’s the pressure of juggling multiple payments while staying financially afloat. No matter the reason, the mental and emotional toll is real and significant.”

Advertisement 4

Article content

Kelley Keehn, a personal finance expert and founder of Money Wise Workplaces, said a no-spend month isn’t a bad idea if it gets people thinking about their finances, but she doesn’t see it as the solution for easing worries about money.

“I’m all for anyone starting somewhere when it comes to their finances. I just worry with trends like this, like a dry January or reboot or those types of things,” she said. “Are you just setting yourself up for this one month that you’re going to try something for a couple of weeks, and then if it fails, you’re going to feel even more guilt and you’re going to feel even more shame?”

Instead, Keehn prefers to focus on the fundamentals to help tackle financial hurdles.

Top amongst those fundamentals is to pay attention to your finances. That means regularly checking your bank account and having the “courage” to write down all your debts and know what the interest rate is on your credit card. Ignoring these things could end up costing you.

Keehn warns that if you miss a credit card payment, it’s possible a rate that was 19.96 per cent could jump to as high as 26 per cent or 29 per cent and stay there until you make payments on time for six months.

Advertisement 5

Article content

Besides staying informed, she also recommends taking a proactive approach and reaching out to your bank if you are having trouble keeping up with things such as credit card payments. The same goes for the Canada Revenue Agency. If you are behind on taxes, call the CRA to see if it can help you figure out a manageable payment plan.

But paying attention is key.

“If you just did that one thing in 2025, you’re going to feel less anxiety and you’re going to feel in more control,” Keehn said. “Even if you feel bad about where you sit, at least now you can get out of it, because no one else is going to help you do that.”

Sign up here to get Posthaste delivered straight to your inbox.

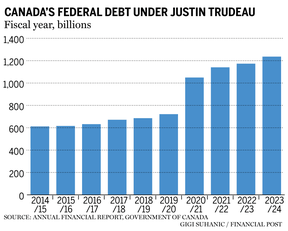

With his party languishing in the polls and under pressure from his caucus, Prime Minister Justin Trudeau announced on Monday that he was resigning as Liberal leader. The decision means Trudeau’s nine-year tenure as Canada’s 23rd leader — a period marked by trade battles with the United States, a global pandemic and high inflation — will end in the coming months. Though Trudeau used his resignation address to defend his record in fighting for the middle class, growing dissatisfaction with his government’s economic policies was a key factor in his declining political fortunes. Here, the Financial Post looks back at 10 key decisions that will shape Trudeau’s economic legacy, for better or worse. — Barbara Shecter and Jordan Gowling, Financial Post

Advertisement 6

Article content

Read the full story here.

- Today’s data: Canada and the U.S. release December jobs data, with the numbers considered key to helping central bankers shape monetary policy in 2025 and decide on the scale and frequency of future rate cuts

- Statistics Canada releases building permits for November

- Earnings: Corus Entertainment Inc., Tilray Brands Inc.

Among the tax changes left in limbo after Justin Trudeau said he is resigning as prime minister that are of most interest to individual taxpayers include the proposed changes to the capital gains tax, and the recent donation deadline extension. Tax expert Jamie Golombek shares his thoughts on a practical approach to each of these unresolved proposed changes. Read more

Calling Canadian families with younger kids or teens: Whether it’s budgeting, spending, investing, paying off debt, or just paying the bills, does your family have any financial resolutions for the coming year? Let us know at wealth@postmedia.com.

Advertisement 7

Article content

McLister on mortgages

Want to learn more about mortgages? Mortgage strategist Robert McLister’s Financial Post column can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Read them here

Financial Post on YouTube

Visit Financial Post’s YouTube channel for interviews with Canada’s leading experts in economics, housing, the energy sector and more.

Today’s Posthaste was written by Gigi Suhanic, with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com.

Recommended from Editorial

-

Posthaste: How the stock market can tank when you least expect it

-

Posthaste: Millennials overtake baby boomers on debt

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.

Article content

How Canadians can ease debt in 2025

2025-01-10 13:00:56